I haven't posted much about the economy lately owing to a time: a lack on my part and the length needed for a post on such a topic. However, a couple of people have made some interesting observations that allow me to weave them together into something that is a little bit more illuminating.

Robert Oak of The Economic Populist and Yves Smith over at Naked Capitalism posted both cited Nouriel Roubini's recent op-ed (here if you don't want to register) in the Financial Times. Mr. Roubini explains that the low interest rates (~0.5%) that the US Federal Reserve is offering to financial institutions is the cause of rapid increase in asset prices (stocks, commodities, etc.) More importantly, since these interest rates have caused the fall in the dollar relative to other currencies. As a result, financial firms are now able to borrow in the US where they get negative interest rates since the dollar is falling, and buy non-US assets which bids up their price. As Gillian Tett of the Financial Times reported recently:

Earlier this month, I received a sobering e-mail from a senior,

recently-retired banker. This particular man, a veteran of the credit

world, had just chatted with ex-colleagues who are still in the markets

– and was feeling deeply shocked.

“Forget about the events of the past 12 months … the punters are

back punting as aggressively as ever,” he wrote. “Highly leveraged

short-term trades are back in vogue as players … jostle to load up on

everything from Reits [real estate investment trusts] and commercial

property, commodities, emerging markets and regular stocks and bonds.“

Back to Roubini. He feels that the increase in asset prices is a new bubble over which the Fed isn't watching. Eventually, the bubble will burst when the dollar stops falling and/or interest rates go up and traders, without easy money from the Fed, find they have the sell their new assets to pay back their loans. Oh joy. Of course, without all that easy money, the financial sector would have imploded taking the rest of the economy with it. Well … more than it did at least.

All this easy money seems to have increased the bounce in the step of Wall Street fat cats such as Lord Griffiths, vice-chairman of Goldman Sachs International, who, while speaking at St Paul’s Cathedral in London about

morality in the marketplace said the British

public should “tolerate the inequality as a way to achieve greater

prosperity for all” (taken from The Guardian via Tony Wikrent of The Economic Populist). Of course we tried that for over thirty years and it hasn't worked.

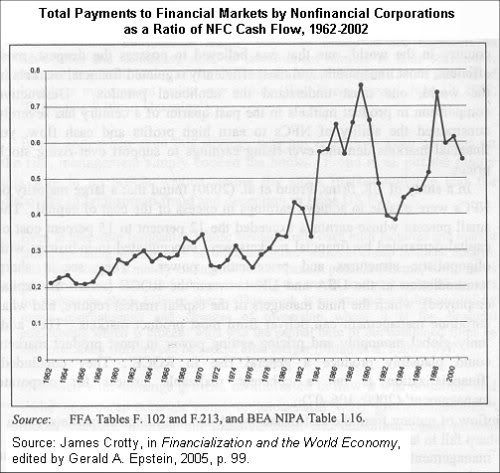

Mr. Wikrent (which I am cribbing from) sets out a fairly detailed description of the financial sector's pillage of the rest of the economy since the early eighties that is pretty well summed up in this graph from a July 2003 paper by Economics Professor James Crotty of the UMass, Amherst, The

Neoliberal Paradox: The Impact of Destructive Product Market

Competition and Impatient Finance on Nonfinancial Corporations in the

Neoliberal Era. The graph shows the share of the cash flow of Non-Financial Corporations (NFC) that went to the financial markets in the form of interest payments, dividends, and stock buy backs:

Yes, that is correct that 75% of NFCs' cash flow in 1989 poured out of NFCs and into the financial markets. Seems suspicious that the financial sector's pillaging of the rest of the economy peaks just before the economy tanks, but I won't take correlation for causation without more information.

For those who want a history, or is it a clarity, lesson, midtowng at The Economic Populist has a pretty good summary of the causes of our latest economic crisis. For those who don't have time to read it, here is the conclusion:

So what does this all mean? It means that the reason for the

economic crisis was the asset bubble that preceded it. The "wealth

effect" was a lie.

The reason for the asset bubble was monetary

inflation that got directed almost entirely to the wealthy. They

naturally used it to become wealthier, which means stocks, bonds, and

real estate. The trickle-down theory is a lie.

The reason why the monetary inflation was directed to the wealthy is

because free trade agreements which gutted the income of the working

class and left the nation suffering from economic disparity. The

promises made by free trade proponents was a lie.

In essence, the economic crisis that we are suffering from, and

will continue to suffer from, was caused by too much concentration of

wealth in the upper class. The country will continue to suffer from

these bubble and bust cycles until either the nation addresses the

income disparity, or the rest of the world stops offering to buy our

debt.

One thing I'll note, while I think NAFTA and other free trade agreements had an

effect on the increase in income inequality, income inequality was

rising long before NAFTA and later free trade agreements. I wouldn't

discount technological changes, the increase in the free flow of

capital and the greediness of the wealthy.

That said, the 50s & 60s era of shared advancements in income and low debt was replaced in the mid 70s with greater income inequality (50% of all income went to the top 10% in 2007) and increasing debt for the middle class and poor in order to achieve some semblance of upward mobility. After all, the rich's new found wealth needed to go someplace to gain a return.

And so I have come full circle with a new bubble on the horizon since that is the only option the "leadership" of our highly unequal economy and political system will allow us.