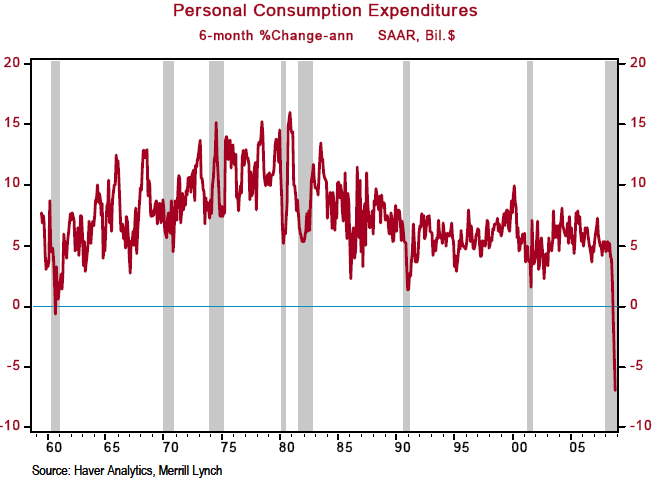

Well, it looks like Obama's financial team has its head just as much in the sand as Bush's team, and more importantly, Japan's team from their ten year financial crisis in the 90s. Tim Duy (by way of Mark Thoma) reports that Obama's plan to deal with financial crisis:

… will be "smaller" than originally expected, said the industry

source, and centered around government guarantees and insurance of troubled

assets …

As the post points out, we tried this with Citigroup and Bank of America, and, at least by the measure of their stock prices, it hasn't worked.

Quick history lesson:

When Japan's asset bubble burst in 1990, many banks were left insolvent with loans that just weren't going to be paid. The Japanese government didn't insist that such banks update their balance sheets to reflect the insolvent loans. On paper the banks were fine, but in reality they were bankrupt. The end result was that these zombie banks lived on for years, suppressing lending and helping to keep the Japanese economy in a recession for ten years.

Apparently we are repeating Japan's mistakes as Tim Duy says:

Classic. Absolutely classic. Is this really addressing the

problem of pricing? Are we not in the same boat of “if we pay too little, the

bank is undercapitalized, but if we pay too much, the taxpayer holds the bag and

therefore we need to nationalize”? Obviously we are in the same boat, because

the new plan may cause an “accounting problem.” Like insolvency. That is, in

fact, a problem, no argument from me. Apparently, though, the Administration’s

solution is a suspension of accounting rules. Translation – we are going to try

to hide the problem.

The solution, of course, is for federal banking regulators to examine banks that look troubled, and nationalize insolvent banks. The share holders get scalped, but what did they expect? Once the feds clean them up, they can then sell them off for a profit when the economy bounces back.

We did this for many savings and loans in the late 80s, but Obama's economics team seems to be avoiding nationalizing troubled banks (Citygroup, BoA, …). Instead, the federal government will guarantee or insure the toxic assets on the bank balance sheets. Heads the banks and their shareholders win, tails the taxpayers lose.

These folks should know they are putting good money after bad, here, but I guess they still believe their precious neoclassical economics more than reality. Its looking like it will be a really long recession, it not something worse.

NOTE: Dollars & Sense has a partial reprint of a Yves Smith article on the same subject. Naked Capitalism has the whole article. Both this one and Tim Duy's are worth the read.